How to Set Up Multiple Bank Accounts for Nonprofit Programs

A practical guide to structuring multiple bank accounts or sub-accounts for nonprofit programs, restricted grants,

Most nonprofits start with a single bank account. It handles everything: donor deposits, grant funds, payroll, vendor payments, and reserves. For a brand-new organization with one funding source and a simple budget, this works fine. But as your nonprofit grows, adds programs, and receives restricted grants, a single account becomes a liability. Funds get commingled, grant compliance becomes difficult, and your board loses visibility into how money is allocated across the organization.

Setting up multiple bank accounts, or sub-accounts within a single banking platform, solves these problems. This guide explains when to separate funds, how to structure your accounts, and how to manage multiple accounts without creating an administrative burden.

Why Nonprofits Need Multiple Accounts

Grant Compliance

Most foundation and government grants come with restrictions on how funds can be spent. A Department of Education grant earmarked for after-school tutoring cannot be used to pay your executive director's salary or cover office rent unless those costs are explicitly included in the approved grant budget. When grant funds sit in the same account as your general operating funds, proving compliance requires meticulous transaction-level tracking.

Separate accounts or sub-accounts for each restricted grant create a clean paper trail. Every deposit into the grant account is grant revenue. Every withdrawal is a grant expense. Your auditor can verify compliance by reviewing the account statements rather than requiring you to trace individual transactions through a commingled general ledger.

Fiduciary Responsibility

Nonprofit boards have a legal obligation to ensure that restricted funds are used for their designated purpose. When all funds are in a single account, the risk of inadvertent misuse increases. Even well-intentioned spending decisions can create compliance issues if restricted funds are accidentally used for unrestricted purposes.

Separating funds into dedicated accounts reduces this risk. Board members can see at a glance how much is available for each purpose, and the organization's financial controls prevent accidental spending across fund boundaries.

Financial Clarity

Multiple accounts provide immediate visibility into your financial position by purpose. Instead of looking at a single balance and trying to mentally subtract restricted funds to determine your actual available operating cash, you can see each balance independently. Your operating account shows what you can spend freely. Your grant accounts show what is committed. Your reserve account shows your safety net.

This clarity is especially valuable for executive directors who need to make spending decisions quickly and for board treasurers who need to report the organization's financial position accurately.

Account Structures That Work

The Basic Three-Account Structure

For nonprofits with annual budgets under $500,000 and one or two restricted funding sources, a three-account structure provides meaningful separation without excessive complexity:

- Operating Account. All unrestricted revenue flows in (general donations, unrestricted grants, earned income). All operating expenses flow out (payroll, rent, utilities, supplies, insurance). This is your primary working account.

- Restricted Funds Account. Restricted grant payments and designated donations are deposited here. Expenses are paid from this account only when they are allowable under the specific restriction. When you have multiple restricted funds, track them through your accounting software using fund codes within this single account.

- Reserve Account. Your operating reserve (typically three to six months of expenses) sits here, earning interest and available for emergencies. This account should rarely have transactions, making it easy to monitor and report on.

The Program-Based Structure

For nonprofits managing multiple programs with distinct funding streams, a program-based structure adds more granularity:

- General Operating Account

- Program A Account (e.g., Youth Education)

- Program B Account (e.g., Community Health)

- Program C Account (e.g., Workforce Development)

- Reserve Account

Each program account receives its allocated funding and pays its direct expenses. Shared costs like rent and administrative salaries are paid from the general operating account, with appropriate allocations recorded in your accounting system.

The Grant-Based Structure

Organizations that receive multiple restricted grants simultaneously may benefit from a grant-based structure:

- General Operating Account

- Federal Grant Account (e.g., HHS Grant 2026-001)

- Foundation Grant Account (e.g., Community Foundation Youth Initiative)

- State Contract Account (e.g., State Dept. of Education Year 3)

- Reserve Account

This approach is most common in organizations subject to federal audit requirements (Uniform Guidance, previously known as OMB Circular A-133) where grant-by-grant tracking is mandatory.

Sub-Accounts vs Separate Bank Accounts

There are two ways to implement a multi-account structure: opening entirely separate bank accounts or using sub-accounts within a single banking platform.

Separate Bank Accounts

How it works: You open individual accounts at one or more banks, each with its own account number, statements, and login credentials.

Advantages: Complete separation of funds, independent FDIC coverage per account (up to $250,000 each), familiar to auditors.

Disadvantages: More administrative overhead, multiple logins to manage, harder to transfer funds quickly between accounts, separate fee structures that can add up, reconciliation across multiple banks is time-consuming.

Sub-Accounts Within One Platform

How it works: Your banking platform creates virtual sub-accounts under a single master account. Each sub-account has its own balance and transaction history but shares a single banking relationship.

Advantages: Single login, instant internal transfers between sub-accounts, unified reporting, typically lower or no additional fees, easier to manage with limited staff.

Disadvantages: FDIC coverage applies to the aggregate balance (though platforms with sweep networks can extend coverage), may not satisfy funders who require a completely separate bank account.

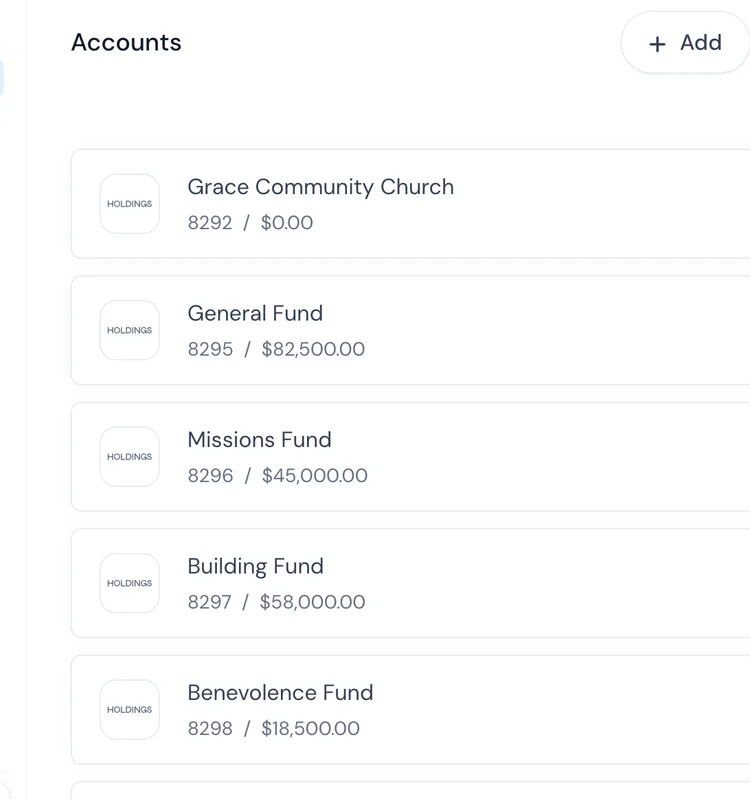

For most nonprofits, sub-accounts provide the organizational benefits of fund separation without the administrative cost of managing multiple banking relationships. Holdings offers unlimited sub-accounts at no additional cost, allowing nonprofits to create dedicated accounts for each grant, program, or designated fund while managing everything through a single dashboard.

Setting Up Your Account Structure

Step 1: Identify Your Fund Categories

Start by listing every distinct pool of money your organization manages:

- General operating funds (unrestricted)

- Each active restricted grant

- Each program with dedicated funding

- Operating reserves

- Capital campaign funds (if applicable)

- Endowment funds (if applicable)

- Fiscal sponsorship funds (if applicable)

Step 2: Determine the Right Level of Separation

Not every fund needs its own bank account or sub-account. Consider these factors:

- Funder requirements. Some grantors require a separate bank account. Check your grant agreements before deciding on sub-accounts.

- Audit requirements. Organizations subject to federal single audits may need more granular separation than those audited under standard nonprofit audit guidelines.

- Volume of transactions. A fund with two transactions per year can be tracked in your accounting software without needing a dedicated bank account. A fund with 50 transactions per month benefits from its own account.

- Staff capacity. More accounts means more reconciliation. Make sure your bookkeeper or finance staff can manage the number of accounts you create.

Step 3: Document Your Account Policies

Create a written policy that describes:

- The purpose of each account or sub-account

- Who is authorized to make deposits and withdrawals from each account

- Approval thresholds for transactions in each account

- How and when internal transfers between accounts are authorized

- How often each account is reconciled

This document becomes part of your financial policies manual and gives auditors confidence that your organization manages restricted funds responsibly.

Step 4: Set Up Accounting Integration

Your accounting system needs to mirror your bank account structure. Each bank account or sub-account should correspond to a fund or account in your chart of accounts. Transactions in the youth education sub-account should automatically map to the youth education fund in your accounting software.

If your banking platform and accounting software integrate directly, this mapping can be automated. If not, you will need to export and import transactions manually, matching each transaction to the correct fund. For guidance on fund accounting software for nonprofits, see our dedicated guide.

Managing Multiple Accounts Effectively

Consolidate Where Possible

More is not always better. If you have ten sub-accounts and three of them have minimal activity, consider consolidating. The goal is to have enough separation for compliance and clarity, but not so much that management becomes a burden.

Automate Internal Transfers

Set up automated transfers for predictable movements of money. For example, if your general operating account funds payroll every two weeks, automate that transfer. If a grant requires quarterly drawdowns, schedule the transfers in advance.

Reconcile Monthly

Every account, whether primary or sub-account, should be reconciled monthly. For organizations with limited finance staff, sub-accounts within a single platform simplify this because all transactions are accessible through one interface.

Review Quarterly with Your Board

Present a consolidated view of all accounts to your board at least quarterly. This should show the balance in each account, the purpose of each account, and any significant transactions or transfers during the quarter. Board members should be able to see that restricted funds are properly segregated and that reserves are at appropriate levels.

Plan for Account Closures

When a grant ends or a program is discontinued, close the associated sub-account after all final expenses have been paid and any remaining funds have been returned to the grantor or transferred according to the grant agreement. Document the closure and archive the account records.

When to Reassess Your Structure

Review your account structure annually or whenever your organization experiences a significant change:

- Receiving a new major restricted grant

- Launching or closing a program

- Changing banking providers

- Preparing for a first-time audit

- Growing past a budget threshold that triggers new compliance requirements

The right structure evolves as your organization grows. What works for a $100,000-budget nonprofit with one grant will not work for a $2 million organization with ten funding sources. Build flexibility into your approach and adjust as needed.

For a comprehensive overview of nonprofit banking, including how to choose the right bank for your account structure, see our nonprofit bank accounts guide.

Related Reading

- [Nonprofit Bank Accounts Guide](/resources/blog/nonprofit-bank-accounts-guide) — Requirements, options, and how to choose the right nonprofit banking partner.

- [Best Bank Accounts for Nonprofits in 2026](/resources/blog/best-bank-accounts-for-nonprofits-2026) — Side-by-side comparison of the top nonprofit banking options.

- [Nonprofit Accounting Software Guide](/resources/blog/nonprofit-accounting-software-guide) — Choosing accounting software that supports fund accounting and grant tracking.

- [Nonprofit Bookkeeping Services Guide](/resources/blog/nonprofit-bookkeeping-services-guide) — When to outsource bookkeeping and what a good engagement looks like.

- [Holdings for Nonprofits](/solutions/nonprofits) — Banking + accounting designed for nonprofit organizations.