Small Business Banking Guide: Everything You Need to Know in 2026

A complete guide to business banking for beginners. Learn why you need a separate business account, what to look for, how to open one, and the mistakes that cost small businesses money.

If you're running a business out of your personal checking account, you're not alone. A surprising number of small business owners — especially early on — just... use their regular bank account for everything. It works fine until it doesn't.

And when it stops working, it usually stops working all at once: a messy tax season, an audit scare, a loan application that requires clean financials you don't have.

This guide covers everything you need to know about business banking — from why you need a separate account to what actually matters when choosing one. No affiliate links, no sponsored rankings. Just the stuff I wish someone had told me when I started my first company.

Why You Need a Separate Business Bank Account

Let's start with the most common question: do you actually need a business bank account?

If you're an LLC, corporation, or partnership — yes, full stop. Mixing personal and business funds can pierce your liability protection. That means the legal separation you set up by forming an LLC could be thrown out in court if someone sues your business and can show you treated it like a personal piggy bank.

If you're a sole proprietor or freelancer, it's technically optional. The IRS doesn't require a separate account. But here's why you should have one anyway:

Clean books at tax time

When every business transaction lives in one account and every personal transaction lives in another, categorizing expenses takes minutes instead of hours. Your accountant (or your software) doesn't have to guess whether that $47 Amazon charge was printer paper or a birthday gift.

Audit protection

If the IRS audits you, they'll want to see clean records. A dedicated business account is the simplest way to show that your business finances are organized and legitimate. Commingled accounts raise red flags.

You look like a real business

Paying vendors and receiving payments from a "John Smith Personal Checking" account doesn't inspire confidence. A business account lets you accept payments under your business name, issue checks that look professional, and generally operate like the business you are.

Easier to track profitability

This one gets overlooked. When your business money is mixed with personal money, you lose the ability to glance at your account and know how the business is doing. A separate account gives you an instant snapshot — money in, money out, what's left.

Types of Business Bank Accounts

There are four main types of business bank accounts. Most businesses need at least one, and many need two or three.

Business checking

This is your operating account — the one you use every day. Money comes in from customers, goes out to vendors, payroll, rent, subscriptions. Every business needs a checking account.

What to look for:

- Low or no monthly fees. Many online banks now offer free business checking. Traditional banks often charge $15-30/month unless you maintain a minimum balance.

- Transaction limits. Some free accounts cap you at 200-500 transactions per month. If you process a lot of payments, check this.

- Integration with your tools. Can it connect to your accounting software? Does it offer an API? This matters more than most people realize.

Business savings

A place to park cash you don't need immediately — tax reserves, emergency funds, future equipment purchases. The main thing here is the interest rate. In 2026, business savings accounts range from 0.01% (most big banks) to 4%+ (online banks and fintech platforms).

The difference is enormous. On a $50,000 balance, that's the difference between earning $5/year and $2,000/year.

Money market accounts

These are a hybrid — higher interest rates than checking, more access than savings. They usually come with check-writing and debit card access but may limit the number of withdrawals per month.

Good for businesses that keep large cash reserves but need occasional access.

Certificates of deposit (CDs)

You lock your money away for a set period (3 months to 5 years) in exchange for a guaranteed interest rate. Useful for funds you know you won't need for a while. Not great for operating cash.

What Actually Matters When Choosing a Business Bank

Here's where most guides fail you. They list 15 banks and give each one a star rating. That tells you nothing about what you should prioritize.

The right bank depends on your business. But here are the factors that matter most, ranked by how much they'll actually affect your day-to-day:

1. Fees (and how to avoid them)

This is the big one. Business bank fees add up fast:

- Monthly maintenance fees: $0-30/month

- Transaction fees: $0.20-0.50 per transaction after your free limit

- Wire fees: $15-30 for domestic wires, $40-65 for international

- Cash deposit fees: Some banks charge for depositing cash beyond a threshold

- Incoming wire fees: Yes, some banks charge you to receive money

The simplest move: choose a bank that doesn't charge monthly fees. These used to be rare for business accounts, but the rise of online banking has changed the game. There's no reason to pay $25/month for a basic checking account in 2026.

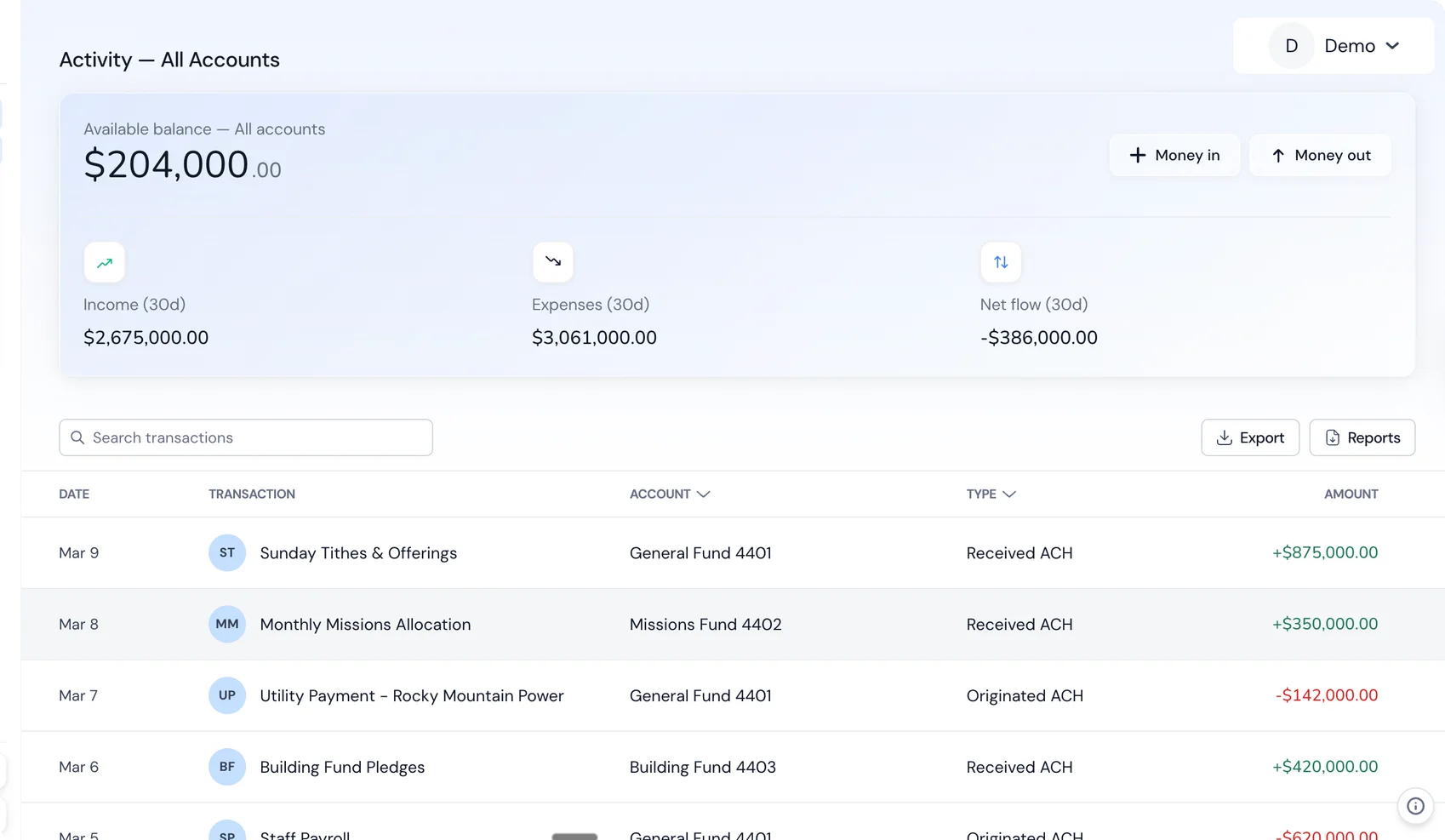

2. Interest on your balance

This is the most overlooked factor in business banking. Most traditional banks pay 0.01% on business checking — effectively nothing. But a growing number of platforms pay 2-4% or more.

If your business maintains an average balance of $30,000, the difference between 0.01% and 3% is roughly $900/year. That's free money you're leaving on the table.

3. Integration with accounting

Your bank account generates the raw data that feeds your books. If that data doesn't flow cleanly into your accounting system, someone (you, your bookkeeper, or your accountant) has to manually enter or reconcile transactions.

Some banks now build accounting tools directly into the banking platform, which eliminates this problem entirely. Your transactions categorize automatically, your P&L updates in real time, and your books are always current.

4. Digital experience

Can you do everything you need to do from your phone or laptop? In 2026, this should be table stakes, but plenty of banks — especially smaller community banks and credit unions — still have clunky digital experiences.

Things that should be easy:

- Send and receive payments

- View transaction history with search and filters

- Download statements

- Manage cards (freeze, set limits, issue virtual cards)

- Set up users with different permission levels

5. Card offerings

You'll want at least a debit card for day-to-day expenses. Virtual cards are increasingly useful for managing subscriptions and online purchases — you can create a unique card number for each vendor, set spending limits, and cancel individual cards without affecting your others.

6. Cash handling

If your business deals with physical cash, you need a bank that makes cash deposits easy. This usually means a traditional bank with local branches. Most online banks don't handle cash well.

If your business is entirely digital (no cash), this doesn't matter — and you can take advantage of the better rates and lower fees that online banks typically offer.

7. Lending and credit

If you'll need a business loan, line of credit, or credit card, some banks make this easier when you already have an account with them. They can see your cash flow history, which makes underwriting faster.

That said, don't choose a bank just because they might lend to you later. You can always get a loan from a different institution.

How to Open a Business Bank Account

The process is straightforward, but having your documents ready will save you time. Here's what you'll typically need:

Documents you'll need

For all business types:

- Employer Identification Number (EIN) — get one free from the IRS website in about 5 minutes

- Personal identification (driver's license or passport)

- Business name and address

For LLCs:

- Articles of Organization

- Operating Agreement (some banks require this)

For corporations:

- Articles of Incorporation

- Corporate bylaws or resolution authorizing the account

For sole proprietors:

- Your Social Security Number (if you don't have an EIN)

- DBA ("Doing Business As") certificate if using a trade name

For partnerships:

- Partnership agreement

The actual process

- Choose your bank. Use the criteria above to narrow it down. Don't agonize — you can always switch later.

- Apply online or in person. Most banks let you apply online in 10-15 minutes. Some may require a branch visit for verification.

- Fund your account. Most banks require an opening deposit — anywhere from $0 to $100. Some require a minimum balance to avoid fees.

- Set up online access. Download the mobile app, enable notifications, and connect any accounting tools.

- Order cards. Get a debit card and set up virtual cards if available.

The whole process usually takes 1-3 business days, though some online banks approve you the same day.

Common Mistakes That Cost Small Businesses Money

After working with hundreds of small businesses, I see the same mistakes over and over. Here are the big ones:

Sticking with your personal bank by default

"I already bank at Chase, so I'll just open a business account there." This is the most common approach, and it's often a mistake. Your personal bank may not offer the best business account. Their business checking might have fees, low interest, poor digital tools, or all three.

Shop around. The 30 minutes you spend comparing options could save you thousands in fees and lost interest over the life of your business.

Ignoring interest rates

Most business owners don't even know what interest rate their business account earns. If the answer is "I don't know" or "basically nothing," you're almost certainly leaving money on the table.

At today's rates, a business with a $50,000 average balance should be earning $1,500-2,000/year in interest. If you're earning less than that, it's worth switching.

Not separating tax reserves

Here's a move that saves small business owners a lot of stress: open a second account (checking or savings) specifically for tax reserves. Every time revenue comes in, move 25-30% to your tax account. When quarterly estimated taxes are due, the money is there. No scrambling, no surprises.

Overcomplicating it

You don't need five bank accounts, three credit cards, and a complex cash management strategy when you're doing $200K in revenue. Start simple: one checking account, maybe a savings account for tax reserves, and a debit card. Add complexity when your business actually needs it.

Choosing a bank for the perks instead of the fundamentals

Free branded checks, a sign-up bonus, or a fancy welcome kit are not reasons to choose a bank. Fees, interest rates, digital experience, and integration with your workflow are reasons to choose a bank. Don't get distracted by the shiny stuff.

When to Upgrade Your Banking Setup

Your banking needs will change as your business grows. Here are the inflection points where most businesses need to level up:

When you hit $10K/month in revenue

At this point, you should definitely have a dedicated business account if you don't already, and you should be paying attention to interest rates. The difference between 0% and 3% starts to matter.

When you hire your first employee

Payroll changes everything. You'll need clean records, and your bank account becomes a critical piece of your financial infrastructure. This is also when you should have proper accounting set up — not a spreadsheet, but real accounting software that tracks income, expenses, and generates the reports you need.

When you start working with an accountant or bookkeeper

They'll need access to your bank data. The easier your bank makes this — through direct feeds, exports, or built-in accounting — the less you'll pay your accountant and the better your books will be.

When you need to prove financial health

Applying for a loan, pitching investors, signing a lease, or bidding on a contract? You'll need clean financial statements. If your banking and accounting are connected, generating these is trivial. If they're not, you're looking at a painful catch-up exercise.

When you're managing multiple accounts or entities

If you have separate accounts for operating expenses, tax reserves, and payroll — or if you're running multiple business entities — you need a banking platform that makes it easy to see everything in one place and move money between accounts.

The Bottom Line

Business banking doesn't have to be complicated. The fundamentals are simple:

- Get a separate account. Don't mix personal and business money.

- Minimize fees. There's no reason to pay monthly maintenance fees in 2026.

- Earn interest. Your idle cash should be working for you.

- Connect your books. Your bank data should flow into your accounting automatically — whether through integrations or a platform that handles both.

- Keep it simple. Start with what you need now, and upgrade when your business tells you to.

The right business bank account saves you time, earns you money, and keeps you organized. The wrong one costs you all three. Take 30 minutes to compare your options — it's one of the highest-ROI things you can do for your business.

Whatever you choose, the most important step is the first one: open the account, move your business transactions over, and start running your business like a business. You'll wonder why you didn't do it sooner.