Business Banking for Freelancers: What You Actually Need (And What You Don’t)

Freelancers don’t need complicated banking. Here’s the minimum viable setup — one account, basic accounting, and a tax reserve — plus when to upgrade.

Freelancers get a lot of conflicting advice about banking. Some say you need a business checking account, a business savings account, a business credit card, a tax savings account, and a separate account for each client. Others say just use your personal account and sort it out at tax time.

Both are wrong. Here's what you actually need.

The Minimum Viable Setup

If you're freelancing — whether you're a designer, developer, writer, consultant, photographer, or any other independent professional — here's the baseline:

1. One Business Bank Account

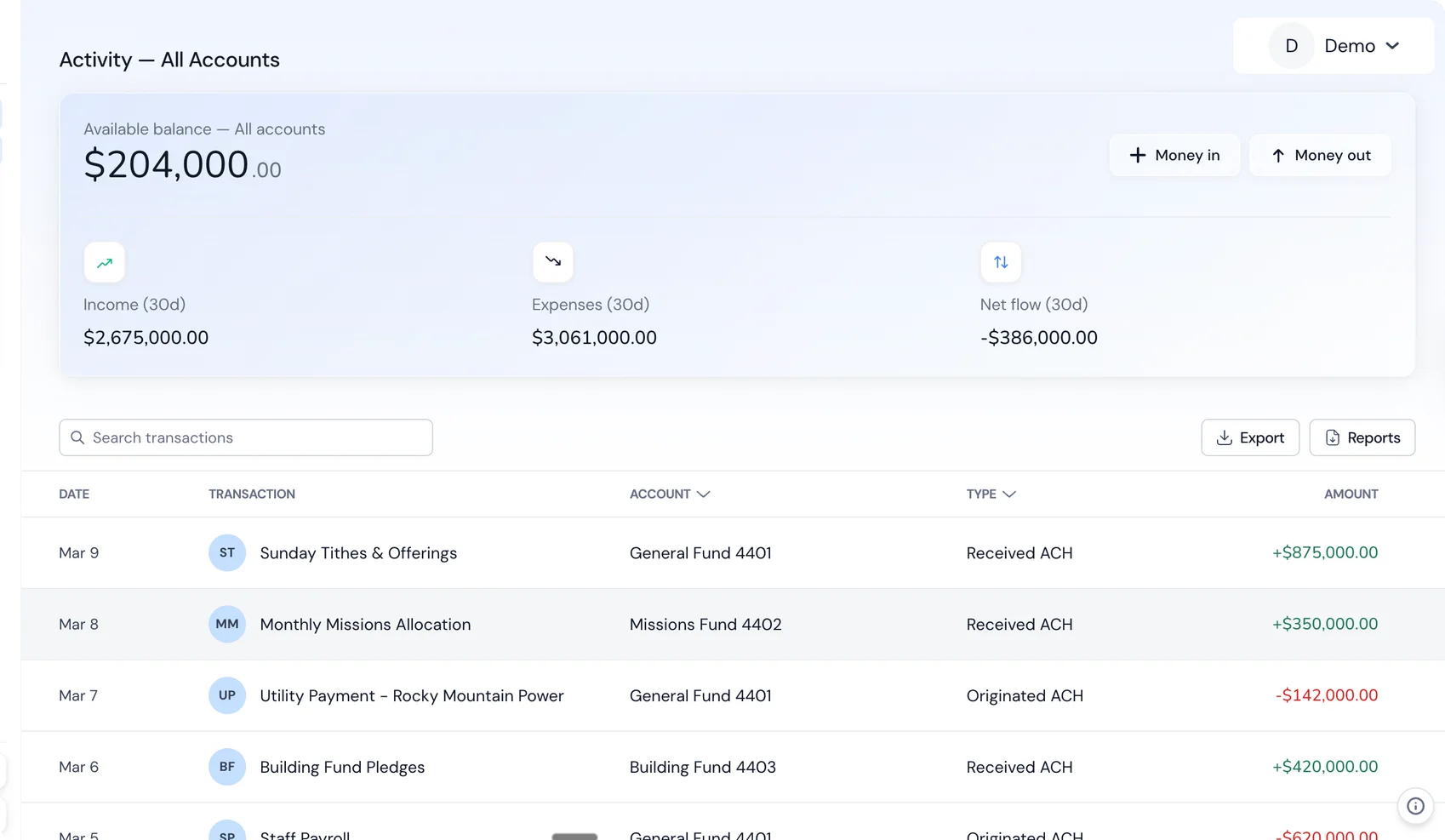

Open a free business checking account. Route all client payments here. Pay all business expenses from here. That's it.

Why not your personal account? Because at tax time, you'll need to identify every business transaction. If business and personal money are in the same account, you're scrolling through Netflix charges and grocery runs to find the Adobe subscription and the client lunch. With a separate account, every transaction is a business transaction by default.

What to look for in a freelancer bank account:

- $0 monthly fees. Your income is variable. Paying $15–$30/month for a bank account doesn't make sense when free options exist. Holdings, Mercury, and Relay all charge nothing for business checking.

- No minimum balance requirements. January might be a $12K month and February might be a $3K month. You shouldn't get penalized with fees because your balance dipped during a slow week.

- Interest on deposits. At 1.75% APY, a $20,000 average balance earns you $350/year. At 0.01% (Chase, Bank of America), you get $2. That's $348/year for choosing the right account.

- Built-in accounting or easy integration. The best freelancer bank accounts auto-categorize transactions — every payment, every expense, sorted into the right bucket without you lifting a finger. If it doesn't have built-in accounting, make sure it integrates cleanly with QuickBooks or Xero.

- Sub-accounts for fund separation. You want at least two buckets: "Operating" and "Tax Reserve." Bonus if you can create more (like "Equipment Fund" or "Vacation Savings") without opening separate accounts.

- Mobile deposit. Clients still send checks. You need to deposit them from your phone, not drive to a branch.

2. A Tax Reserve Sub-Account

This is the part most new freelancers get wrong — and it leads to a panicked scramble every April.

Set aside 25–30% of every payment you receive into a tax reserve. Quarterly estimated taxes are non-negotiable for freelancers earning over ~$1,000/year — the IRS charges penalties if you underpay.

What percentage should you reserve? It depends on your total income and tax bracket:

| Total Annual Income | Federal Bracket | Self-Employment Tax | State Tax (avg) | Total Reserve % |

|---|---|---|---|---|

| Under $44,725 | 12% | 15.3% | ~5% | 25% |

| $44,726–$100,525 | 22% | 15.3% | ~5% | 30% |

| $100,526–$191,950 | 24% | 15.3% | ~5% | 30–33% |

| Over $191,950 | 32%+ | 15.3% (capped) | ~5% | 33–40% |

The self-employment tax (15.3%) is the one that surprises people. As a W-2 employee, your employer pays half of Social Security and Medicare. As a freelancer, you pay both halves. On $100K in freelance income, that's $15,300 just in self-employment tax — before federal and state income tax.

The easiest approach: create a sub-account within your business bank called "Tax Reserve." Set up an automatic rule: when money comes in, move 30% to the reserve. Pretend that money doesn't exist until estimated taxes are due (April 15, June 15, September 15, January 15).

3. A Business Debit Card

Use it for all business purchases. Software subscriptions, co-working space, client meals, equipment, travel. This creates an automatic paper trail for deductions. Leave the personal card for personal expenses.

Why a debit card over a credit card? For most freelancers starting out, a debit card is simpler. No credit application, no annual fee, no risk of carrying a balance. Once your income stabilizes above $75K and you want to build business credit or earn rewards, adding a business credit card makes sense. But it's not where you start.

That's It. Seriously.

You don't need:

- A separate savings account — unless your checking pays 0% and you want to earn interest on reserves.

- A business credit card — nice to have for building business credit, but not required.

- Multiple bank accounts — one account with sub-accounts covers most freelancers until you're well into six figures.

- An LLC — beneficial for liability protection, but not required to open a business bank account. Most banks let sole proprietors open a business account with just an SSN and a government ID.

What to Track (And How)

Freelancers have simpler books than most businesses. You need to track:

- Revenue: Every client payment, listed by client

- Expenses: Every business purchase, categorized (software, travel, meals, equipment, home office, etc.)

- Estimated tax payments: When you paid, how much, to which agency (federal + state)

- Mileage (if applicable): Business miles driven, with date and purpose

If your bank includes accounting software, most of this happens automatically. Transactions are categorized as they flow through. You review monthly to make sure the categories are right, and you're done.

The Monthly Financial Review (30 Minutes)

Block 30 minutes on the last day of each month. Here's your checklist:

Revenue check:

- Total revenue this month vs. last month. Trending up or down?

- Revenue by client — are you over-dependent on one client? If more than 50% of your income comes from one source, you have a concentration risk.

- Outstanding invoices — who owes you money, and how overdue is it?

Expense check:

- Review every transaction category. Does anything look off?

- Cancel any subscriptions you're not using. (The average freelancer is paying for 2–3 unused tools at any given time — that's $50–$150/month in waste.)

- Check for any personal expenses that accidentally went through the business card.

Tax reserve check:

- What's the balance in your tax reserve sub-account?

- Is it on track for the next quarterly payment? Quick math: take your year-to-date profit, multiply by your reserve percentage, divide by 4. That's roughly what each quarterly payment should be.

- When is the next quarterly payment due?

Cash flow forecast:

- What's coming in next month? (Signed contracts, recurring clients, pending invoices)

- What's going out? (Recurring expenses, any large purchases planned)

- Will you need to adjust your owner's draw?

This monthly review takes 30 minutes and prevents 90% of the financial surprises freelancers face. Do it consistently and you'll always know where you stand.

The Common Freelancer Tax Deductions

These are the categories most freelancers can deduct. Make sure your accounting tracks them:

| Category | Examples | Common Mistakes |

|---|---|---|

| Software & tools | Adobe CC ($55/mo), Figma ($15/mo), GitHub ($4/mo), hosting ($20/mo), domains ($12/yr) | Forgetting annual renewals; not tracking free-trial-to-paid conversions |

| Home office | Percentage of rent/mortgage, utilities, internet based on dedicated office space | Claiming the deduction without a dedicated space; not measuring the space |

| Equipment | Computer ($1,500), monitor ($400), camera ($800), desk ($300), chair ($250) | Not knowing you can deduct the full cost under Section 179 instead of depreciating over years |

| Professional development | Courses ($200–$2,000), books ($100–$300/yr), conferences ($500–$3,000), certifications | Not keeping receipts for online courses; forgetting conference travel expenses |

| Travel | Flights, hotels, rental cars for client or business travel | Not separating personal days on mixed trips; not logging the business purpose |

| Meals (50% deductible) | Client lunches ($30–$80), meals while traveling for business | Forgetting to note who you met with and the business purpose — the IRS requires this |

| Marketing | Website hosting ($15/mo), portfolio site, business cards ($50), advertising ($100–$500/mo) | Lumping marketing and software into one category |

| Professional services | Accountant ($500–$2,000/yr), lawyer ($300–$1,000/yr), bookkeeper ($100–$200/mo) | Not deducting tax prep fees |

| Health insurance | Self-employed health insurance premiums (deducted on personal return, not Schedule C) | Trying to deduct it on Schedule C instead of the front of Form 1040 |

| Retirement contributions | SEP IRA (up to 25% of net self-employment income), Solo 401(k) (up to $23,500 + 25% employer match) | Not contributing at all — a $10K SEP IRA contribution at the 24% bracket saves $2,400 in taxes |

| Mileage | Standard rate of $0.70/mile for 2026 (check IRS annually) | Not keeping a mileage log — the IRS disallows the entire deduction without contemporaneous records |

Home office deduction — simplified vs. actual method:

The simplified method is $5 per square foot, up to 300 square feet. Maximum deduction: $1,500. Easy to calculate, no receipts needed for home expenses.

The actual method calculates the percentage of your home used for business (office square footage ÷ total home square footage) and applies that percentage to actual expenses: rent/mortgage interest, utilities, insurance, repairs, depreciation. If your office is 150 sq ft in a 1,500 sq ft apartment, that's 10% of your $2,000/month rent ($200/month = $2,400/year), plus 10% of utilities, internet, etc. This usually produces a larger deduction than the simplified method, but requires more record-keeping.

Equipment depreciation vs. Section 179:

When you buy a $2,000 laptop, you have two options. Under standard depreciation, you'd deduct a portion each year over 5 years ($400/year). Under Section 179, you deduct the full $2,000 in the year you bought it. For most freelancers, Section 179 is the better choice — you get the full tax benefit immediately. Just know it exists so you're not slowly depreciating your desk over 7 years when you could've written it off day one.

The Quarterly Tax Workflow

If you're earning more than about $1,000/year from freelancing, you're expected to pay estimated taxes quarterly. Here's the step-by-step process:

When Payments Are Due

| Quarter | Covers Income From | Due Date |

|---|---|---|

| Q1 | January 1 – March 31 | April 15 |

| Q2 | April 1 – May 31 | June 15 |

| Q3 | June 1 – August 31 | September 15 |

| Q4 | September 1 – December 31 | January 15 (next year) |

Yes, the quarters aren't actually equal. Q2 covers 2 months and Q3 covers 3. Don't ask us why — that's the IRS for you.

How to Calculate Your Payment

The simple method (safe harbor): Pay 100% of last year's total tax liability, divided by 4. If you owed $20,000 last year, pay $5,000 per quarter. Even if you earn more this year, you won't owe penalties as long as you've paid at least 100% of last year's tax (110% if your AGI was above $150,000).

The precise method: Calculate your actual income each quarter, apply your effective tax rate (federal income tax + self-employment tax + state), and pay that amount. This is more accurate but more work. Use IRS Form 1040-ES or your accounting software's tax estimate feature.

How to Pay

- Go to irs.gov/payments

- Choose "Make a Payment"

- Select "Estimated Tax" and the correct quarter

- Pay via bank account (free), debit card ($2.50 fee), or credit card (1.85% fee)

- Save the confirmation number

- Don't forget state estimated taxes — most states have their own quarterly payment system

What Happens If You Miss a Payment

The IRS charges an underpayment penalty — currently around 7% annually on the underpaid amount. If you owed $5,000 for Q1 and paid nothing, the penalty is roughly $87.50 for that quarter (7% × $5,000 × 3 months / 12). It compounds, so missing multiple quarters gets expensive. The penalty is calculated per-quarter, so paying late is better than not paying at all.

Miss an entire year of estimated taxes on $100K of freelance income, and you could owe $1,500–$2,000 in penalties on top of the tax itself. Not catastrophic, but completely avoidable.

When to Upgrade Your Setup

Your minimum viable setup works until it doesn't. Here are the specific triggers:

Revenue exceeds $75K/year. At this level, you should be working with a CPA (not doing your own taxes) and considering whether an LLC or S-Corp election would save you money. An S-Corp election can save $3,000–$8,000/year in self-employment tax once your profit exceeds $80K — but it requires running payroll, which adds complexity and cost ($30–$50/month for a service like Gusto).

Revenue exceeds $150K/year. Time for a monthly bookkeeper ($100–$300/month). At this income level, a bookkeeper pays for themselves in caught deductions and clean financial statements. You should also be doing monthly P&L reviews and quarterly financial planning.

You're hiring subcontractors. Once you're paying other people, you need to track 1099 payments, and your books get more complex. Any freelancer paying contractors more than $600/year needs to issue 1099-NEC forms — and your bank/accounting setup needs to support that tracking.

You've formed an LLC or S-Corp. Different entity types have different accounting requirements. S-Corps require you to run payroll for yourself. LLCs with multiple members need formal operating agreements and potentially separate capital accounts. Your one-account-with-sub-accounts setup still works, but the accounting behind it gets more sophisticated.

You have multiple revenue streams. Freelance income plus course sales plus affiliate revenue plus consulting — each needs separate tracking for an accurate P&L by revenue line. Sub-accounts help here: create one per revenue stream so you can see which parts of your business are actually profitable.

You're thinking about a business loan. Lenders want to see 12–24 months of clean financial statements ��— P&L, balance sheet, and bank statements. If your books are a mess, start cleaning them up at least 6 months before you apply. A bookkeeper can help you produce the kind of statements that make lenders say yes.

When to form an LLC: The common advice is "when you have something to protect." More specifically: when your freelance income exceeds $50K/year, when you're signing contracts with significant liability exposure (consulting for companies where your advice could lead to financial loss), or when you're working with clients who require it. Formation costs $50–$500 depending on your state, plus annual fees in some states ($0 in most, up to $800 in California).

Frequently Asked Questions

Do freelancers need a business bank account?

Legally, sole proprietors aren't required to have one. Practically, you absolutely should. It makes taxes easier, creates cleaner records, and separates your business from your personal finances. Many accounts are free — there's no reason not to.

Should I form an LLC to freelance?

An LLC provides liability protection (your personal assets are shielded from business lawsuits) and can have tax advantages. Whether the benefit justifies the cost ($50–$500 to form depending on state, plus annual fees in some states) depends on your risk exposure and income level. Most freelancers earning over $50K/year should at least consider it. If you're a consultant giving advice that companies act on, the liability protection is especially valuable.

How much should I set aside for taxes?

25–30% of gross income is a safe starting point for most freelancers. This covers federal income tax, self-employment tax (15.3%), and state income tax. If you're in a high-tax state (California, New York), lean toward 30–35%. If you're in a no-income-tax state (Texas, Florida, Washington), you might get away with 25%.

Can I deduct my home office?

Yes, if you have a dedicated space used exclusively for business. The simplified method is $5/square foot up to 300 sq ft ($1,500 max deduction). The regular method calculates the percentage of your home used for business and applies it to rent, utilities, insurance, etc. You need a space that's used only for work — the dining table where you also eat dinner doesn't count.

Do I need to send invoices from my business bank account?

No — invoices are separate from your bank. But your invoice should list your business name and include payment instructions that direct to your business bank account. Using invoicing software (or your bank's built-in invoicing) creates a professional paper trail and makes it easy to match payments to invoices.

What's the best bank for freelancers in 2026?

Look for: $0 fees, interest on deposits (1.5%+ APY), built-in or integrated accounting, sub-accounts, and no minimum balance. Holdings checks all of those boxes. Mercury and Relay are also solid options. Traditional banks (Chase, BofA, Wells) charge fees and pay essentially nothing in interest — they're designed for large businesses, not freelancers.

---

Holdings is built for freelancers who want to keep it simple — free banking, free accounting, 1.75% APY, and sub-accounts for tax reserves. [Get started →](/banking)

---